5 Key Tech Priorities for Fintech Leaders in 2024

- Cara May-Cole

- 25th Jan 2024

- 10 min of reading time

In the fast-paced world of financial tech, staying on top isn’t just about seeing ahead—it’s also about committing to evolving strategies. For CTOs leading the charge, we’re taking a closer look at the 5 key things they should focus on in 2024, building on what we talked about in 2023.

If you caught our last piece, you’ll know the landscape has changed, bringing in new challenges and opportunities that need a fresh perspective.

In 2024, big changes are happening in fintech, particularly with cryptocurrencies. Evolving past speculation they’re becoming a big part of regular financial systems, shaking up the way of doing things in finance.

At the same time, businesses are getting on board with using cryptocurrencies for everyday transactions. This shift is blurring the lines between old-school finance and the new digital finance wave, making global financial systems more flexible and connected.

Countries like China, Sweden, South Korea, the US, and the European Union are taking the lead in exploring and possibly launching Central Bank Digital Currencies (CBDCs). The goal? To make transactions cheaper, include more people in the financial system, and revolutionise how we make payments across borders.

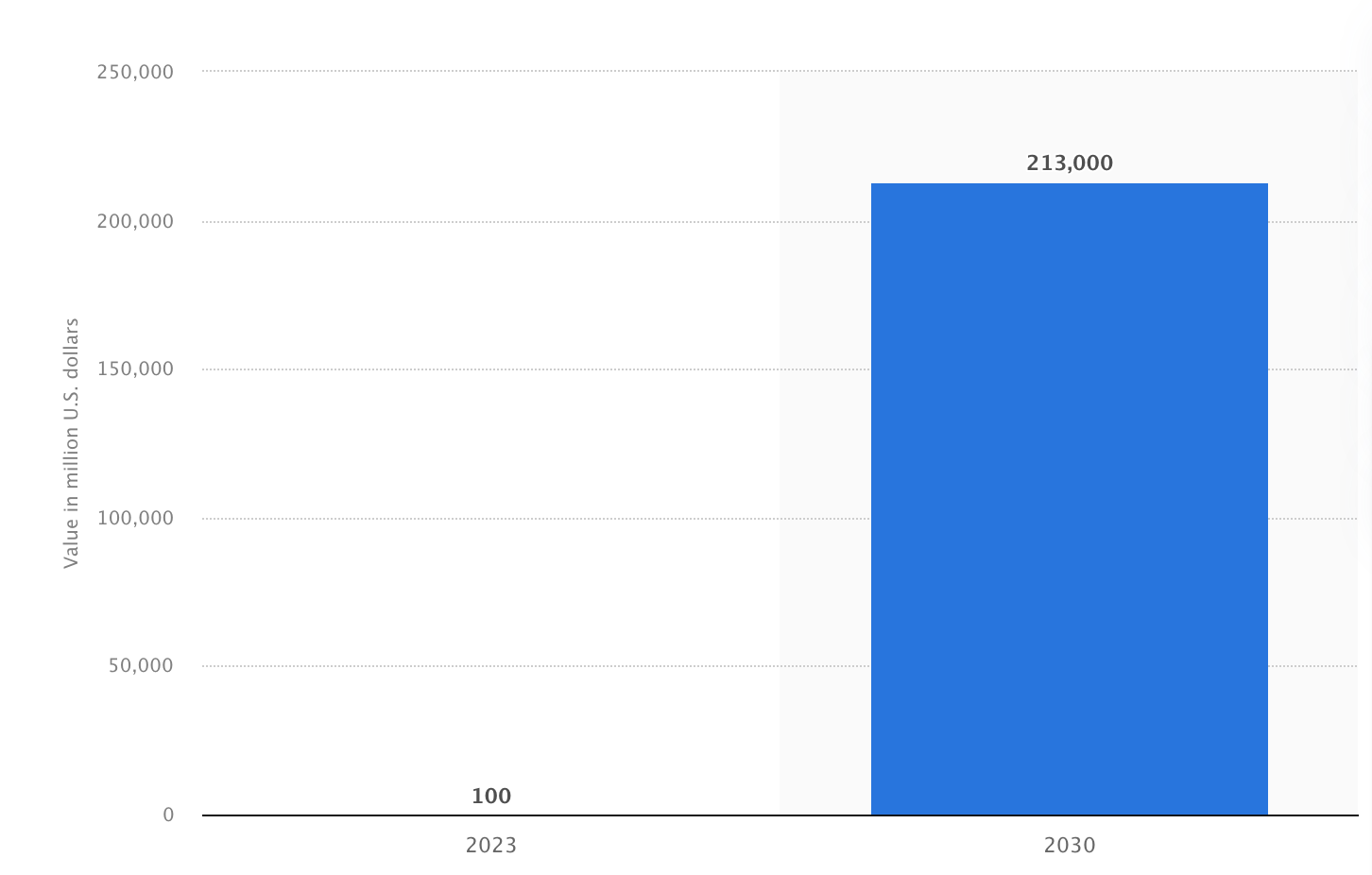

Market size of central bank digital currency (CBDC) worldwide in 2023, with a forecast for 2030, Statistica

For fintech companies, this is a golden opportunity to be the go-to partner for those navigating these changes. They can use innovative solutions, especially in infrastructure, security, custody, data management, market analytics, and transaction monitoring.

Jumping back to 2023, a turning point for CBDCs. Many countries tested them out, and some are already using them. The European Central Bank is gearing up for its digital euro project after two years of digging into it. According to a study by Juniper Research, we’re looking at a whopping $213 billion processed through CBDCs by 2030, showing how much they’re set to grow. Looking specifically at 2024, Juniper further predicts more specific uses, like cross-border payments and business transactions.

Why the focus on CBDCs? They offer a stable and reliable digital currency, especially when you compare them to the crazy ups and downs of other cryptocurrencies. So for CTOs navigating these changes, it’s time to get your companies ready to ride the wave of digital currencies.

We’ve mentioned the increasing popularity of Central bank digital currencies (CBDCs). At the same time, embedded finance is transforming how financial services are integrated into non-financial platforms.

This means users can access banking, payments, and other financial features without leaving the apps they’re using. For example, services like Buy Now Pay Later (BNPL) are gaining traction among younger consumers, even though they come with risks like debt accumulation. Despite these challenges, BNPL transactions are expected to grow significantly from $120 billion in 2021 to $576 billion by 2026.

Embedded finance is spreading beyond traditional sectors, with banking services now available in e-commerce and ride-hailing apps. Even companies like Tesla are getting in on the action by offering insurance with their car purchases. However, as we approach 2024, the convenience of embedded finance also brings challenges, especially concerning data privacy and security.

Despite this, the combination of central bank digital currencies and embedded finance is undeniably reshaping the current landscape. The rise of digital currencies reflects a shift in how transactions are done, while embedded finance is changing how users interact with financial services. This presents both opportunities and challenges for businesses, and as CTOs, understanding and adapting to these trends will be crucial for staying ahead in fintech innovation.

This surge of digital currencies and central banks is particularly driven by the maturation and expansion of decentralised finance (DeFi).

DeFi is in a transformative phase, refining lending and borrowing protocols while bringing innovative features to decentralised exchanges. The shift towards DeFi is part of a broader effort to democratise financial services, offering an enriched array of choices beyond conventional banking. As we enter this new era of financial engagement, the collaboration between fintech and DeFi projects is noteworthy. Fintech companies, recognising the potential impact, are contributing expertise and resources to make DeFi more accessible, secure, and user-friendly.

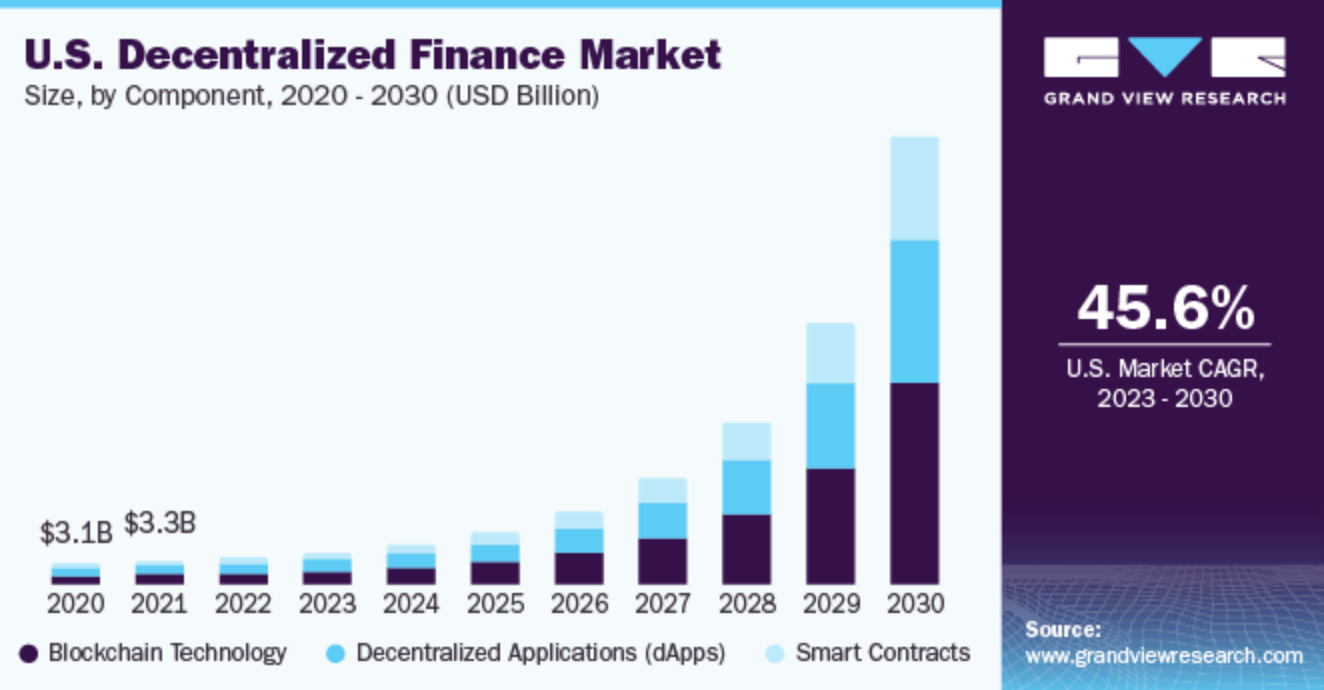

On the quantitative front, Grand View Research valued the decentralised finance market at 13.61 billion USD in 2022, with projections indicating a substantial revenue increase to 231.19 billion USD by 2030. These numbers underscore the exponential growth and significance of DeFi in reshaping the financial landscape.

Decentralised Finance Market (in USD)

2024 marks a pivotal moment where CTOs can leverage technological expertise to navigate the complexities of central bank digital currencies and the expanding DeFi ecosystem. Embracing these changes strategically can position organisations at the forefront of fintech, fostering innovation and resilience in rapid transformation.

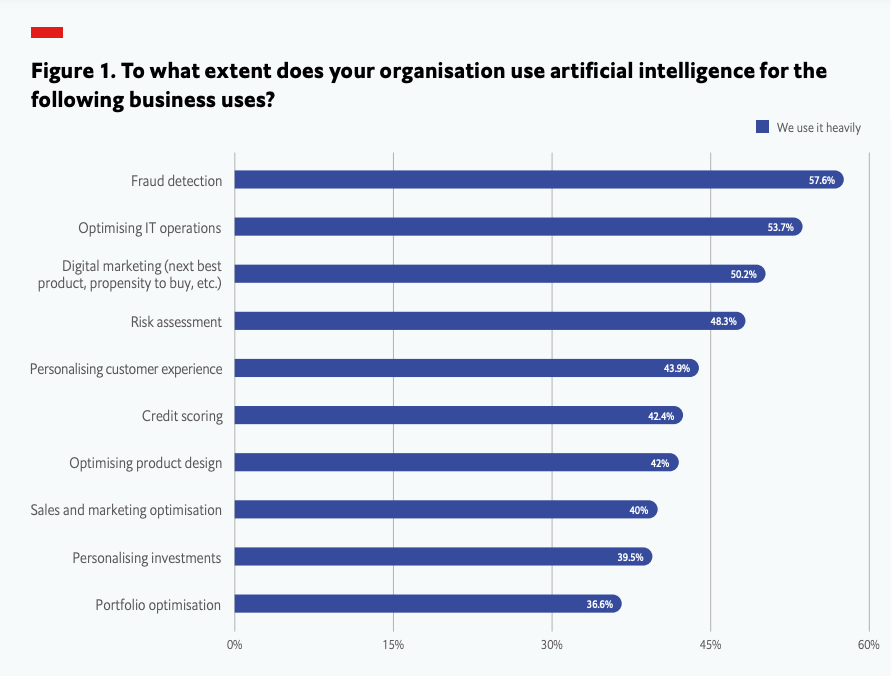

The integration of artificial intelligence (AI) and machine learning (ML) is redefining financial services. Artificial intelligence is already rapidly advancing, with innovations like ChatGPT, DALL-E, and Midjourney transforming how businesses approach technology. AI and ML are poised to disrupt various sectors this year, particularly fintech, leading to notable developments in how financial technology is advanced and adopted. A notable study by The Economist reveals that 52% of traditional banks are already leveraging both artificial intelligence and machine learning for various business functions, as shown below:

The Economist Unit Survey

AI is predominantly employed by banks for fraud detection, with 58% heavily relying on it and an additional 32% using it to some extent. Similarly, in optimising IT operations, 54% utilise AI extensively, while 36% employ it to some extent.

Virtually all banks currently incorporate AI to some degree or have plans to do so within the next three years, spanning various business domains such as operations and customer experience. The upcoming areas for substantial growth encompass personalised investments, with 17% planning adoption in the next 1-3 years, followed by credit scoring (15%) and portfolio optimisation (13%).

Customised services that are set to further impact financial behaviours will include:

Managing risk

AI tools enable businesses to analyse and improve regulatory approaches, shifting from reactive to proactive risk management.

Enhancing Customer Experience:

Fintech leveraging AI for customer experience gains a competitive edge by offering personalised financial services, AI-driven automation, chatbots, and virtual assistants to anticipate user needs, providing real-time, tailored support, and financial guidance.

Automation in Fintech:

AI-driven automation in Fintech goes beyond routine tasks, handling complex decision-making flows like loan approvals, improving efficiency, and reducing operational costs.

AI and Blockchain Synergy:

Integration of AI with blockchain enhances the security, transparency, and scalability of financial transactions, particularly in smart contracts.

Transforming Payments with AI:

AI-powered payment solutions offer faster, more secure transactions, with machine learning analysing user behaviour for personalised experiences and biometric authentication.

Modernising Traditional Financial Services with AI:

AI applications in traditional financial services include customer service automation, fraud detection, and personalised portfolio management.

The upcoming year is set to play a crucial role in the continuous advancement and incorporation of technologies driven by artificial intelligence. Fintech firms, although capable of enhancing efficiency and capabilities, must collectively prioritise values such as transparency, fairness, and user-centricity.

In 2024, biometric authentication is reshaping how we secure finances. It uses unique traits like fingerprints and faces, along with newer methods like voice recognition. This approach simplifies user interactions, doing away with traditional PINs and passwords.

Alongside this, identity trends for the year include improving Single Sign-On (SSO) with added security features and the rise of decentralised identity systems using blockchain. Cloud-based Identity-as-a-Service (IDaaS) is also growing for scalable and cost-effective solutions.

Guidance from regulations is essential. Striking a balance between convenience and privacy, robust data protection is also crucial. In summary, 2024 is a key time for financial security, making transactions safer and smoother. CTOs should navigate these changes, embracing advancements while handling regulatory challenges.

In the ever-evolving landscape of fintech, the priorities for CTOs are not static but fluid, responding to dynamic shifts in technology and consumer behaviour. The challenges and opportunities of 2024 underscore the need for CTOs to exhibit adaptability and strategic foresight.

If you want to start a conversation about engaging us for your fintech project or talk about partnering and collaboration opportunities, don’t hesitate to contact the Erlang Solutions team. We seamlessly prototype, build, monitor, and maintain mission-critical solutions for payment systems, digital lending, clearing and settlement services, and more. Trusted by industry leaders like Klarna, Vocalink (Mastercard), Visa, Danske Bank, and Safaricom, our consultative approach, combined with our teams expertise, ensures that businesses can confidently direct their resources toward strategic goals and growth.

Márton Veres shares his journey and what he’s looking forward to in his new role as London Business Unit Leader.

Avoid common startup tech mistakes that slow growth. Build a stack that scales from day one.

Digital wallet security is essential as mobile payments grow. Understand the risks and how to keep your business and customers safe.