7 Key Blockchain Principles for Business

- Erlang Solutions Team

- 30th May 2024

- 19 min of reading time

Welcome to the final instalment of our Blockchain for Business series. Here, we are taking a look at the seven fundamental principles that make blockchain: Immutability, decentralisation

‘workable’ consensus, distribution and resilience, transactional automation (including ‘smart contracts’), transparency and trust, and links to the external world.

For business leaders, understanding these core principles is crucial in harnessing the potential for building trust, spearheading innovation and driving overall business efficiency.

If you missed the previous blog, feel free to learn all about the strengths of Erlang and Elixir in blockchain here.

Now let’s discuss how these seven principles can be leveraged to transform business operations.

In a survey conducted by EY, over a third (38%) of US workers surveyed said that blockchain technology is widely used within their businesses. A further 44% said the tech would be widely used within three years and 18% reported that they were still a few years away from being widely used within their business.

To increase the adoption of blockchain, it is key to understand its principles, how it operates, and the advantages it offers across various industries, such as financial services, retail, advertising and marketing, and digital health.

In an ideal world, we would want to keep an accurate record of events and make sure it doesn’t degrade over time due to natural events, human error, or fraud. While physical items can change over time, digital information can be continuously corrected to prevent deterioration.

Implementing an immutable blockchain aims to maintain a digital history that remains unaltered over time. This is especially useful for businesses when it comes to assessing the ownership or the authenticity of an asset or to validate one or more transactions. In the context of legalities and business regulation, having an immutable record of transactions is key as this can save time and resources by streamlining these processes.

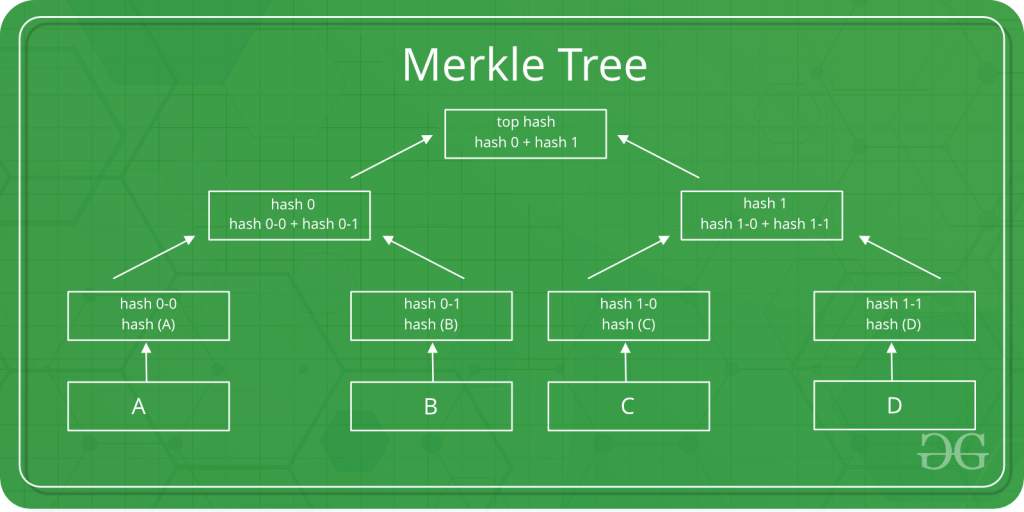

In a well-designed blockchain, data is encoded using hashing algorithms. This ensures that only those with sufficient information can verify a transaction. This is typically implemented on top of Merkle trees, where hashes of combined hashes are calculated.

In a well-designed blockchain, data is encoded using hashing algorithms. This ensures that only those with sufficient information can verify a transaction.

Legitimate questions can be raised by business leaders about storing an immutable data structure:

Businesses face challenges in managing growing data, maintaining decentralisation, verifying transactions, and preventing risks in immutable data storage. Meeting regulations also add complexity, and deciding what data to store must consider sensitivity.

Compliance with GDPR introduces challenges, especially concerning the “right to be forgotten.” This is important because fines for breaches of GDPR are potentially very severe for non-compliance. The solutions introduced so far effectively aim at anonymising the information that enters the immutable on-chain storage process, while sensitive information is stored separately in support databases where this information can be deleted if required.

The challenge lies in determining upfront what information is considered sensitive and suitable for inclusion in the immutable record.. A wrong choice has the potential to backfire at a later stage if any involved actor manages to extract or trace sensitive information through immutable history.

Immutability in blockchain technology provides a solution to preserving accurate historical records, ensuring the authenticity and ownership of assets, streamlining transaction validation, and saving businesses time and resources. But it also has its challenges, such as managing data volumes, maintaining decentralisation, and ensuring it is complying with regulations, for example, GDPR. Despite these challenges, businesses can leverage immutable blockchain technology to modernise record-keeping practices and uphold the integrity of their operations.

Remember the 2008 financial crash? One of the reactions following this crisis was against over-centralisation.

In response to the movement towards decentralisation, businesses have acknowledged the potential for innovation and adaptation. Embracing decentralisation not only aligns with consumer values of independence and democratic fairness, but it also presents opportunities for businesses to explore new markets and develop innovative products and services, as well as implement decentralised governance models within their own organisations.

There are many ways in which businesses can leverage blockchain technology in order to embrace decentralisation and unlock new growth opportunities:

Decentralised finance (DeFi): DeFi platforms leverage blockchain technology to provide financial services without the need for intermediaries, such as banks or brokerages.

Supply chain management: By recording every transaction on a blockchain ledger, businesses can track the movement of goods from the point of origin to the end consumer.

Smart contracts: Automatically enforce and execute contractual agreements when predefined conditions are met, also without the need for intermediaries.

Tokenisation of assets: Businesses can turn their assets into digital tokens. This helps split ownership into smaller parts, making it easier to buy and sell, and allowing direct trading between people without intermediaries.

Identity management: Blockchain-based identity management systems offer secure and decentralised solutions. Businesses can use blockchain to verify the identity of customers, employees, and partners while giving people greater control over their data.

Data management and monetisation: Blockchain allows for businesses to securely manage and monetise data by giving individuals control over their data, facilitating direct transactions between data owners and consumers.

With full decentralisation, there is no central authority to resolve potential transactional issues. Traditional, centralised systems have well-developed anti-fraud and asset recovery mechanisms which people have become used to.

Using new, decentralised technology places a far greater responsibility on the user if they are to receive all of the benefits of the technology, forcing them to take additional precautions when it comes to handling and storing their digital assets.

There has no point in having an ultra-secure blockchain if one then hands over one’s wallet private key to an intermediary whose security is lax: it’s like having the most secure safe in the world and then writing the combination on a whiteboard in the same room.

For businesses, embracing decentralisation unlocks new opportunities while posing challenges in security and usability. Balancing these factors is key as businesses continue to navigate decentralised technologies, shaping the future of commerce and industry.

Businesses must consider whether the increased level of personal responsibility associated with secure blockchain implementation is a price users are willing to pay, or if they will trade off some security for ease of use and potentially more centralisation.

As businesses are increasingly pushing towards decentralised forms of control and responsibility, it has since been brought to light the fundamental requirement to validate transactions without a central authority; known as the ‘consensus’ problem. The blockchain industry has seen various approaches emerge to address this, with some competing and others complementing each other.

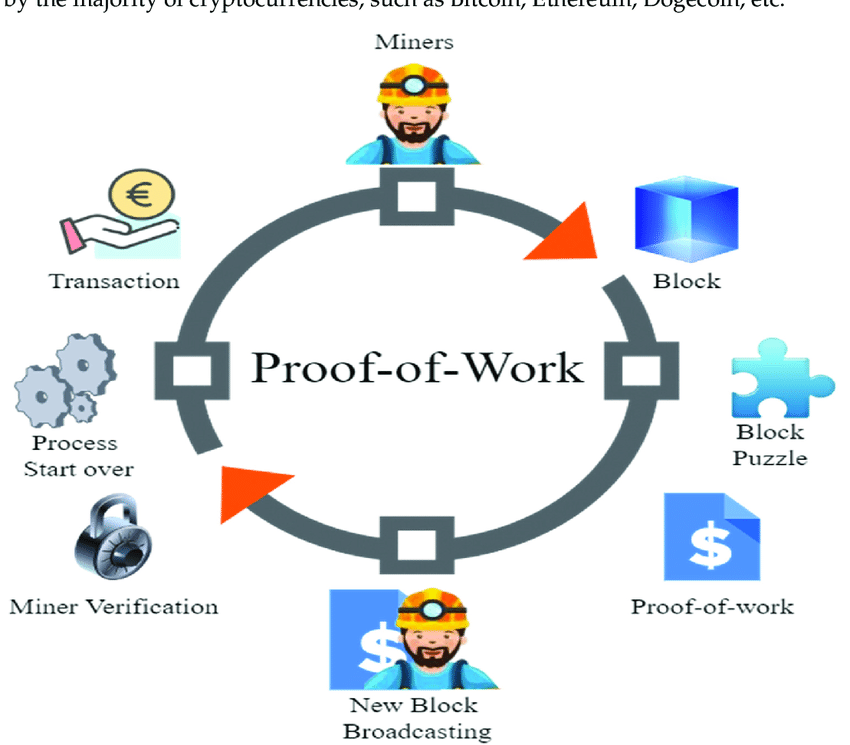

There’s been a lot of attention on governance in blockchain ecosystems. This involves regulating how quickly new blocks are added to the chain and the rewards for miners (especially in proof-of-work blockchains). Overall, it’s crucial to set up incentives and deterrents so that everyone involved helps the chain grow healthily.

Besides serving as an economic deterrent against denial of service and spam attacks, Proof of Work (POW) approaches are amongst the first attempts to automatically work out, via the use of computational power, which ledgers/actors have the authority to create/mine new blocks. Similar approaches (proof of space, proof of bandwidth etc) have followed, but all of them are vulnerable to deviations from the intended fair distribution of control.

How do these methods benefit businesses? It gives them an edge by purchasing powerful hardware in bulk and running it in areas with cheaper electricity. This can help to outpace competitors in mining new blocks and gaining control, ultimately centralising authority.

In response to the challenges brought on by centralised control and environmental concerns associated with traditional mining methods, alternative approaches such as Proof of Stake (POS) and Proof of Importance (POI) have emerged. These methods remove the focus from computing resources and tie authority to accumulated digital asset wealth or participant productivity. However, implementing POS and POI while mitigating the risk of power and wealth concentration could present significant challenges for developers and business leaders alike.

Apart from decentralising authority, control and governance, blockchain solutions typically embrace a distributed peer-to-peer (P2P) design paradigm.

This preference is motivated by the inherent resilience and flexibility that these types of networks have introduced and demonstrated, particularly in the context of file and data sharing. A centralised network, typical of mainframes and centralised services is exposed to a ‘single point of failure’ vulnerability as the operations are always routed towards a central node.

If the central node breaks down or is congested, all the other nodes will be affected by disruptions. In a business context, decentralised and distributed networks attempt to reduce the detrimental effects that issues occurring on a node might trigger on other nodes. In a decentralised network, the failure of a node can still affect several neighbouring nodes that rely on it to carry out their operations. In a distributed network the idea is that the failure of a single node should not impact significantly any other node. Even when one preferential/optimal route in the network becomes congested or breaks down entirely, a message can still reach the destination via an alternative route.

This greatly increases the chance of keeping a service available in the event of failure or malicious attacks such as a denial of service (DOS) attack. Blockchain networks with a distributed ledger redundancy are known for their resilience against hacking, especially when it comes to very large networks, such as Bitcoin. In such a highly distributed network, the resources needed to generate a significant disruption are very high, which not only delivers on the resilience requirement but also works as a deterrent against malicious attacks (mainly because the cost of conducting a successful malicious attack becomes prohibitive).

Although a distributed topology can provide an effective response to failures or traffic spikes, businesses need to be aware that delivering resilience against prolonged over-capacity demands or malicious attacks requires adequate adapting mechanisms. While the Bitcoin network is well positioned, as it currently benefits from a high capacity condition (due to the historically high incentive to purchase hardware by third-party miners), this is not the case for other emerging networks as they grow in popularity. This is where novel instruments, capable of delivering preemptive adaptation combined with back pressure throttling applied to the P2P level, can be of great value.

Distributed systems are not new and, whilst they provide highly robust solutions to many enterprise and governmental problems, they are subject to the laws of physics and require their architects to consider the trade-offs that need to be made in their design and implementation (e.g. consistency vs availability).

A high degree of automation is required for businesses to sustain a coherent, fair and consistent blockchain and surrounding ecosystem. Existing areas with a high demand for automation include those common to most distributed systems. For example; deployment, elastic topologies, monitoring, recovery from anomalies, testing, continuous integration, and continuous delivery.

For blockchains, these represent well-established IT engineering practices. Additionally, there is a creative R&D effort to automate the interactions required to handle assets, computational resources and users across a range of new problem spaces (e.g. logistics, digital asset creation and trading).

The trend of social interactions has seen a significant shift towards scripting for transactional operations. This is where smart contracts and constrained virtual machine (VM) interpreters have emerged – an effort pioneered by the Ethereum project.

Many blockchain enthusiasts are drawn to the ability to set up asset exchanges, specifying conditions and actions triggered by certain events. Smart contracts find various applications in lotteries, digital asset trading, and derivative trading. However, despite the exciting potential of smart contracts, getting involved in this area requires a significant level of expertise. Only skilled developers who are willing to invest time in learning Domain Specific Languages (DSL) can create and modify these contracts.

The challenge is to respond to safety and security concerns when smart contracts are applied to edge case scenarios that deviate from the ‘happy path’. If badly designed contracts cannot properly roll back or undo a miscarried transaction, their execution might lead to assets being lost or erroneously handed over to unwanted receivers.

Another area in high need of automation is governance. Any blockchain ecosystem of users and computing resources requires periodic configurations of the parameters to carry on operating coherently and consensually. This results in a complex exercise of tuning for incentives and deterrents to guarantee the fulfilment of ambitious collaborative and decentralised goals. The newly emerging field of ‘blockchain economics’ (combining economics; game theory; social science and other disciplines) remains in its infancy.

The removal of a central ruling authority produces a vacuum that needs to be filled by an adequate decision-making body, which is typically supplied with automation that maintains a combination of static and dynamic configuration settings. Those consensus solutions referred to earlier which use computational resources or social stackable assets to assign the authority, not only to produce blocks but also to steer the variable part of governance, have succeeded in filling the decision-making gap in a fair and automated way. Successively, the exploitation of flaws in the static element of governance has hindered the success of these models. This has contributed to the rise in popularity of curated approaches such as POA or DPOS, which not only bring back centralised control but also reduce the automation of governance.

This a major area of evolution in blockchain where we expect to see major widespread market adoption.

For businesses to produce the desired audience engagement for blockchain and eventual mass adoption and success, consensus and governance mechanisms need to operate transparently. Users need to know who has access to what data so that they can decide what can be stored and possibly shared on-chain. These are the contractual terms by which users agree to share their data. As previously discussed, users might be required to exercise the right for their data to be deleted, which typically is a feature delivered via auxiliary, ‘off-chain’ databases. In contrast, only hashed information, effectively devoid of its meaning, is preserved permanently on-chain.

Given the immutable nature of the chain history, it is important to decide upfront what data should be permanently written on-chain and what gets written off-chain. The users should be made aware of what data gets stored on-chain and with whom it could potentially be shared. Changing access to on-chain data or deleting it goes against the fundamentals of immutability and therefore is almost impossible. Getting that decision wrong at the outset can significantly affect the cost and usability (and therefore likely adoption) of the particular blockchain in question.

Besides transparency, trust is another critical feature that users and customers legitimately seek. Trust has to go beyond the scope of the people involved as systems need to be trusted as well. Every static element, such as an encryption algorithm, the dependency on a library, or a fixed configuration, is potentially exposed to vulnerabilities.

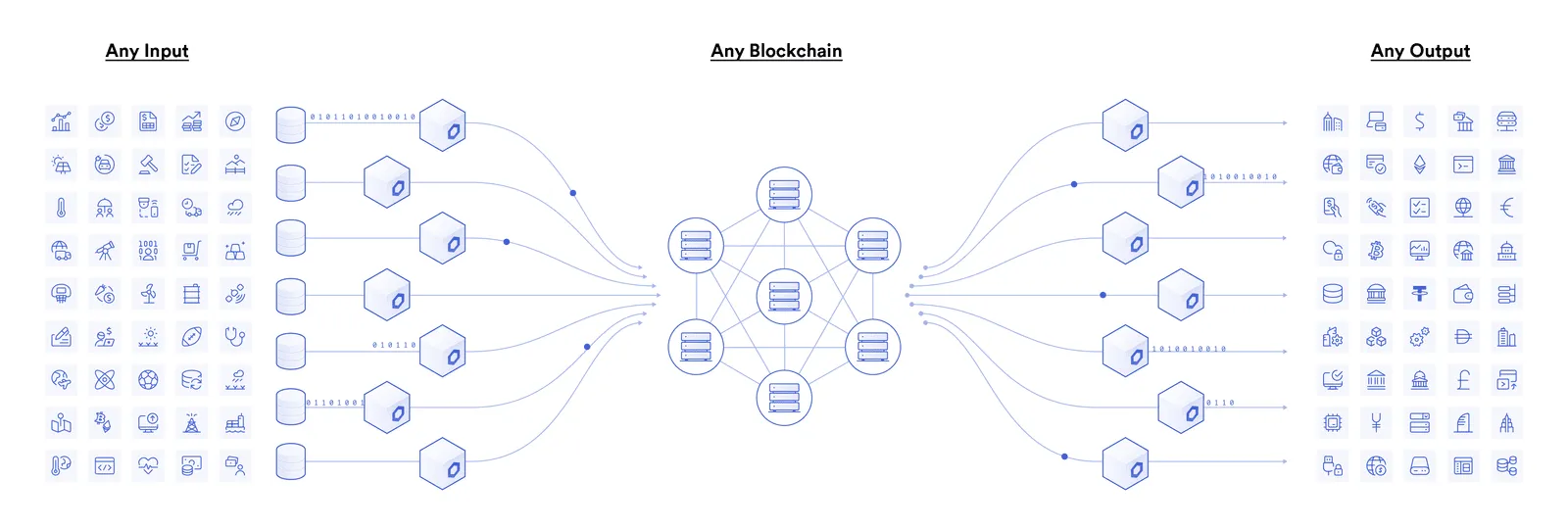

The attractive features that blockchain has brought to the internet market would be limited to handling digital assets unless there was a way to link information to the real world. Embracing blockchain solely within digital boundaries may diminish its appeal, as businesses seek solutions that integrate seamlessly with the analogue realities of our lives.

Technologies used to overcome these limitations include cyber-physical devices such as sensors for input and robotic activators for output, and in most circumstances, people and organisations. As we read through most blockchain white papers, we occasionally come across the notion of the Oracle, which in short, is a way to name an input coming from a trusted external source that could potentially trigger/activate a sequence of transactions in a Smart Contract or which can otherwise be used to validate some information that cannot be validated within the blockchain itself.

Blockchain oracles connecting blockchains to inputs and outputs

Bitcoin and Ethereum, still the two dominant projects in the blockchain space are viewed by many investors as an opportunity to diversify a portfolio or speculate on the value of their respective cryptocurrencies. The same applies to a wide range of other cryptocurrencies except fiat pegged currencies, most notably Tether, where the value is effectively bound to the US dollar. Conversions from one cryptocurrency to another and to/from fiat currencies are normally operated by exchanges on behalf of an investor. These are again peripheral services that serve as a link to the external physical world. For businesses, these exchanges provide crucial services that facilitate investment and trading activities, contributing to the broader ecosystem of blockchain-based assets.

Besides oracles and cyber-physical links, interest is emerging in linking smart contracts together to deliver a comprehensive solution. Contracts could indeed operate in a cross-chain scenario to offer interoperability among a variety of digital assets and protocols. Although attempts to combine different protocols and approaches have emerged, this is still an area where further R&D is necessary to provide enough instruments and guarantees to developers and entrepreneurs. The challenge is to deliver cross-chain functionalities without the support of a central governing agency/body.

As we’ve highlighted throughout the series, blockchain provides real transformative potential across varying business industries. For a business to truly leverage this technology, the fundamentals we have highlighted must be understood to navigate the complexities of blockchain adoption successfully.

If you want to start a conversation with the team, feel free to drop us a line.

Blog series of thinking from Erlang Solutions’ subject matter experts on blockchain technology from software engineering principles to how Erlang and Elixir can help you innovate in the space.

Our take on 2021 use cases of blockchain in financial services as we get ready for our sponsored session on the topic as part of Fintech Week London 2021.

Read how Vocalink, Goldman Sachs, SumUp and Solaris are using Erlang and Elixir BEAM languages in their tech stack.